A Roth Individual Retirement Account (IRA) allows you to put money away long-term. If you follow the rules, your distributions during retirement are tax-free. If you are eligible to contribute to a Roth IRA, it can become a powerful retirement savings vehicle.

How Does A Roth IRA Work?

With a Roth IRA, you deposit funds that have already been taxed. You don’t get to deduct the contribution from your income as you do with a traditional IRA contribution. However, if you wait to take withdrawals until you are 59 1/2 years old or the account has been around for five years, whichever is later, the distributions are tax-free.

Traditional IRAs require you to begin taking withdrawals and paying tax on them, at age 72. However, Roth IRAs have no minimum distributions. You can let them grow tax-free during your lifetime and, if you are fortunate enough to not spend them, you can pass them on to your heirs tax-free as well.

If you need to take funds out of a Roth IRA prior to age 59 1/2 or before the account has been around for five years, the GROWTH (not your contribution) is taxed as income and is penalized 10%.

For example, You put $6,000 in the account this year and invested it. A year later, the account has reached $7,000 and you empty it out. Your original $6,000 would be yours to take, tax and penalty-free. However, the $1,000 growth would be taxed at your marginal tax rate and penalized. So you don’t necessarily want to put the funds in planning to pull them back out. But if you had to withdrawal your original contribution in a pinch you can do so.

Note: Under certain circumstances, withdrawals will be taxed but not subject to the 10% penalty. This includes:

- Distributions to cover higher education expenses

- unreimbursed medical expenses

- health insurance premiums while unemployed

- to cover part of a first-time home purchase

Who is Eligible for a Roth IRA?

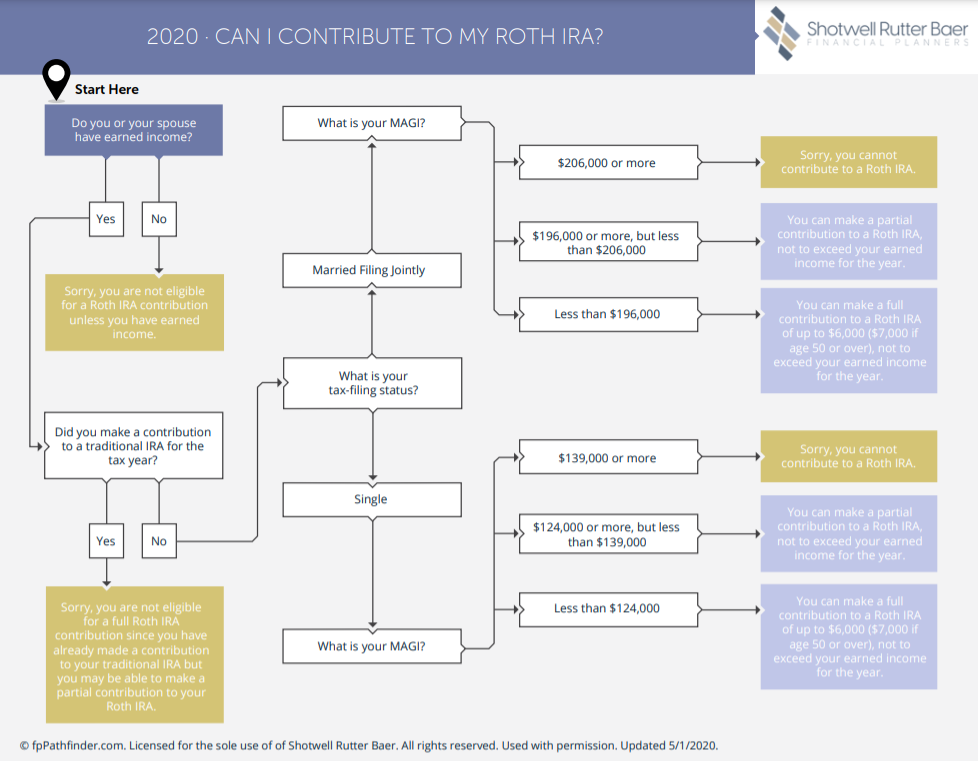

To be eligible to make a Roth IRA contribution in a particular year, you first must have earned income. Second, for 2020, your modified adjusted gross income must be:

- less than $196,000 if you are married and file a joint tax return, or

- less than $124,000 if you are single.

If you make more than those amounts, you can make a partial Roth contribution up until your modified adjusted gross income reaches $206,000 for married filers and $139,000 for single taxpayers.

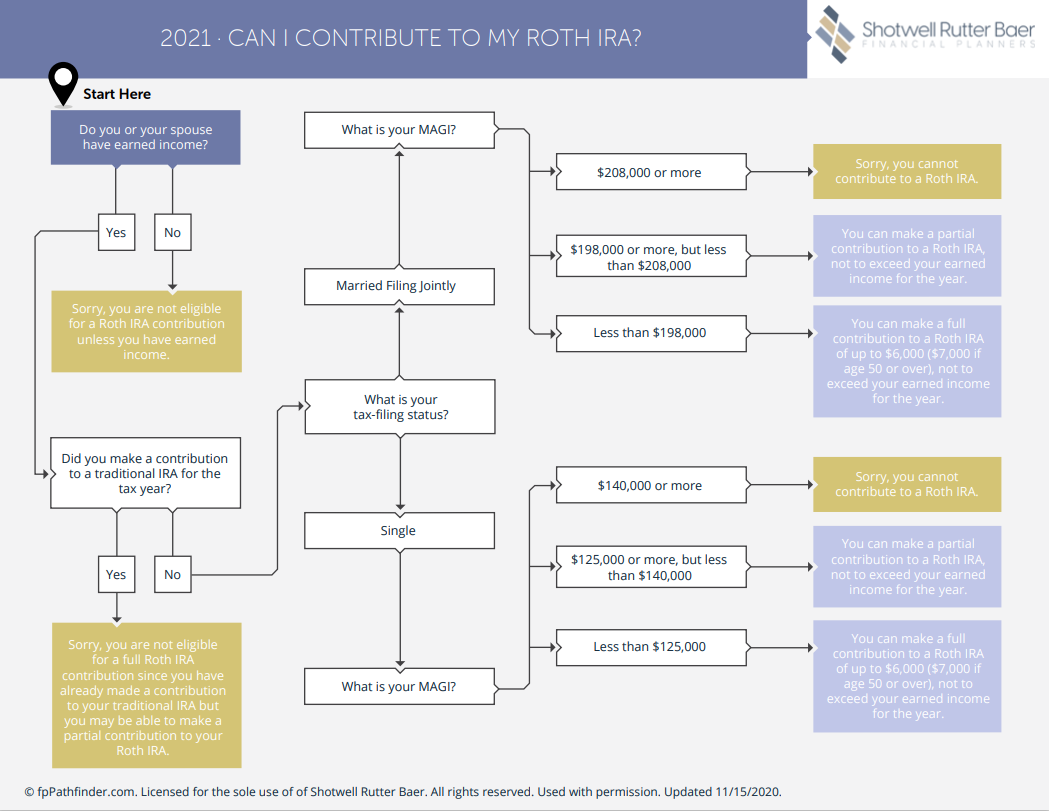

Above those limits, you aren’t allowed to make a Roth contribution. For 2021 contributions, these limits all adjust upward for inflation. For single-filers, they adjust by $1000 and for joint-filers by $2000. See the eligibility charts below for 2020 and 2021.

How Much Can I Contribute?

Provided you are below the limits outlined above, for 2020 and 2021 you can contribute 100% of your earned income up to $6,000 per year if you are 49 or younger, and up to $7,000 per year if you are 50 or older.

When is a Roth IRA a Good Idea?

A Roth IRA is a good idea if you are in a lower tax bracket (say 22% or less) and have excess savings or cash-flow that can be set aside for the long-term, like retirement. You are essentially “locking in” your current low tax rate in anticipation that taxes might be higher later in your life. In general, I would advise savers to contribute to their employer retirement plan to get all of their employer’s matching funds before saving in a separate Roth IRA (note also that many 401k plans now have a Roth option built into them). Since you can take your contributions back out at any time without tax or penalty, the risks of tying up the funds are relatively low. Keep in mind that these vehicles are best used for long-term savings.

If you anticipate that you will be in a lower tax bracket later in life, during retirement, you may be better off making a traditional, deductible IRA contribution instead of a Roth. That might also be true in years when your earned income is still low enough to allow for a Roth contribution, but some other circumstance, say investment income or a property sale, might put you in a higher tax bracket.

How Do I Set Up A Roth IRA?

Any investment advisor or online investment company should be able to open a Roth IRA for you. You will need to provide your personal information, including your Social Security Number, to create the account. You will also want to name beneficiaries for the account in case something happens to you.

Once set up, you can contribute to the account however you see fit. Some clients prefer a regular, monthly contribution, while others prefer to deposit a lump sum. Since Roth IRAs are not generally funded directly from your paycheck, you can control the deposits. Note that you can make a contribution for a particular year up until you file your taxes for that year. So a 2020 contribution can be made up until April 15, 2021, or October 15, 2021, if you get an extension for your return.

What Investments Go in a Roth IRA?

Once set up, you can invest in just about any publicly traded stock, bond, or mutual fund, or even money markets and certificates of deposit if you open your Roth at a bank. I recommend diversified mutual funds as the best way to go for most clients. Because Roth IRAs are generally long-term investment vehicles, I encourage people to take some risk with their Roth IRA while young as extra risk should lead to better returns over the long-haul. When in doubt, Target Date Retirement Funds are often a good, simple choice.

About Shotwell Rutter Baer

Shotwell Rutter Baer is proud to be an independent, fee-only registered investment advisory firm. This means that we are only compensated by our clients for our knowledge and guidance — not from commissions by selling financial products. Our only motivation is to help you achieve financial freedom and peace of mind. By structuring our business this way we believe that many of the conflicts of interest that plague the financial services industry are eliminated. We work for our clients, period.

Click here to learn about the Strategic Reliable Blueprint, our financial plan process for your future.

Call us at 517-321-4832 for financial and retirement investing advice.

Podcast: Play in new window | Download