S5E4 – State of Michigan Retirement Benefits

Podcast: Play in new window | Download

Understanding State of Michigan Retirement Benefits: Pension vs. Defined Contribution and Health Care Options

If you work for the State of Michigan, your retirement benefits can feel like a maze. Hire dates matter. Plan elections matter. Even health care decisions from years ago still matter today.

In this episode of Kitchen Table Finance, Nick and Dave sit down at the table to break it all down in practical, everyday language. We walk through how to figure out what plan you are in, what your options mean, and how to think about retirement income and health care with clarity and confidence.

If you have ever looked at your benefits statement and thought, where do I even start, this conversation is for you.

Watch the full episode HERE.

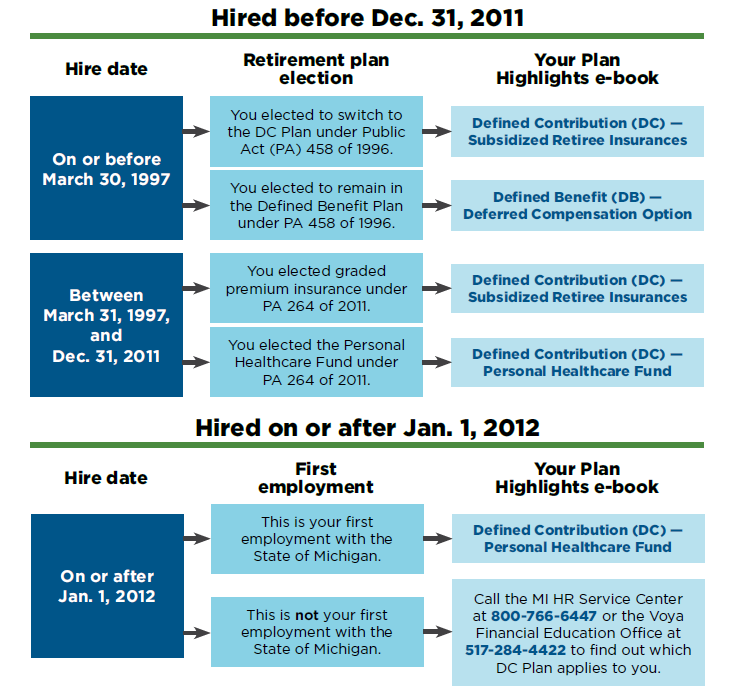

How to Determine Which Retirement Plan You Are In

The first step is understanding your hire date and whether you made any elections when changes were introduced in 1997 and 2011.

The three primary categories are:

- Defined Benefit Pension Plan

- Defined Contribution with Subsidized Retiree Insurance

- Defined Contribution with Personal Health Care Fund

Nick and Dave walk through how these plans evolved over time and why your employment history determines which system you fall into. When in doubt, the Michigan Office of Retirement Services can confirm your status.

Defined Benefit Pension Plan Explained

A defined benefit plan provides a lifetime monthly income based on a formula. Your pension is typically calculated using:

- Final average compensation

- Pension multiplier

- Years of service

You do not manage investments inside the pension. The State assumes the investment risk, and you receive a steady payment for life.

We also discuss spousal election options, how benefits are reduced based on survivor coverage, and how to think through those decisions as part of a broader retirement plan.

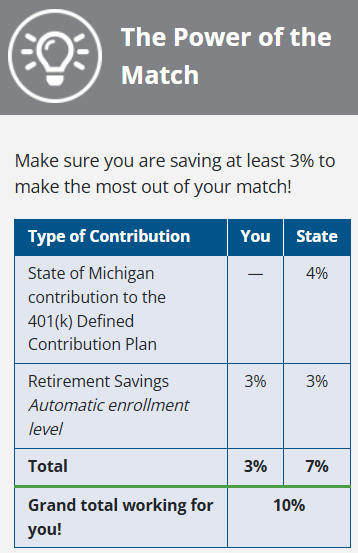

Defined Contribution Plan Overview

A defined contribution plan works more like a 401k. You contribute a percentage of your salary, and the State provides a match.

The structure generally includes:

- 4 percent automatic State contribution

- 100 percent match on up to 3 percent employee contribution

From there, your retirement outcome depends on contributions, investment performance, and distribution strategy.

We also cover:

- Traditional vs. Roth 401k contributions

- The 457 plan and its early withdrawal flexibility

- In plan Roth conversions

- Investment options through Voya

- The self directed brokerage window through Schwab

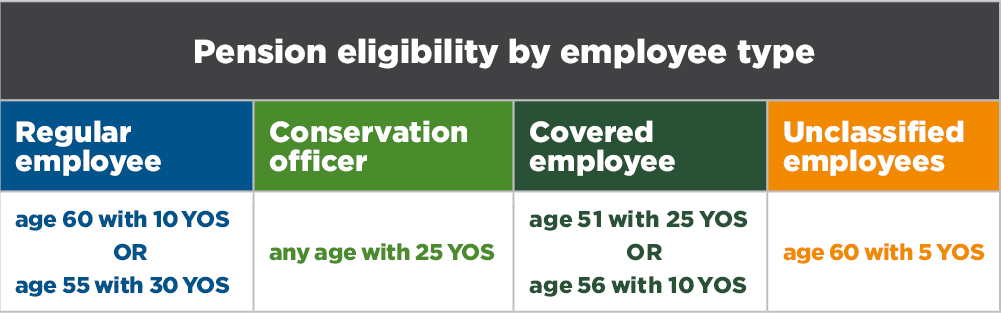

Vesting Rules You Need to Know

For pension participants, full vesting typically requires:

- Age 60 with 10 years of service

- Or age 55 with 30 years of service

For defined contribution participants:

- Your contributions are always 100 percent vested

- Employer contributions vest 50 percent after 2 years

- 75 percent after 3 years

- 100 percent after 4 years

Understanding vesting is critical if you are considering a career change before retirement.

Retiree Health Care: What Changes in Retirement

Health care is one of the biggest retirement stress points, especially for those retiring before Medicare.

There are two primary paths:

Subsidized Retiree Insurance

The State continues to offer coverage in retirement and pays a percentage of your premiums based on your service years.

This provides guaranteed coverage and predictable cost sharing, which can bring peace of mind for many retirees.

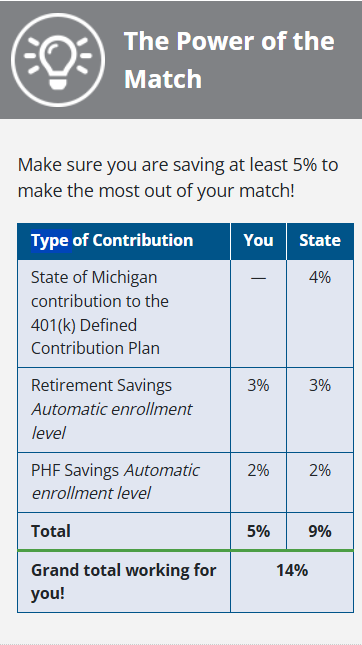

Personal Health Care Fund

Instead of subsidized insurance, the State contributes additional money into your defined contribution account.

You are responsible for securing your own coverage, whether through:

- The health care marketplace before age 65

- Medicare and supplemental coverage after age 65

We discuss why health insurance planning today is more flexible than it was 15 years ago and how proper planning can reduce the stress around this decision.

Key Takeaways from This Episode

- Your hire date drives your retirement structure

- Pension and defined contribution plans operate very differently

- Health care decisions significantly impact retirement cash flow

- Early retirement requires careful coordination of 401k and 457 rules

- Working with a fiduciary planner can help you avoid costly mistakes

State of Michigan retirement benefits are complex, but they are manageable with the right guidance and a clear strategy.

If you would like help understanding how your benefits fit into your overall retirement plan, we are here to help.

Contact SRB today at 517-321-4832 or email us at info@srbadvisors.com.

Don’t forget to subscribe to our channel for more bite-sized financial and retirement tips.

Other Podcasts Referenced in This Episode

Share post: