The debt ceiling debate has been front and center lately, so we thought we’d share this article from our partners at Clearnomics discussing this issue and how it may impact markets. Over the past week, there has been nonstop news coverage of the federal government hitting the $31.4 trillion borrowing limit known as the debt ceiling. This once again puts Washington drama on center stage as the Treasury Department enacts “extraordinary measures” to not default on its obligations. Although this has become a regular occurrence, many investors are still understandably nervous. While it’s unclear how this will play out politically before the estimated June 5 deadline, the fortunate news is that financial markets have taken these events in stride. How can long-term investors maintain the right perspective around political and fiscal uncertainty in spite of these headlines?

Watch on YouTube HERE

The federal government has hit the debt ceiling

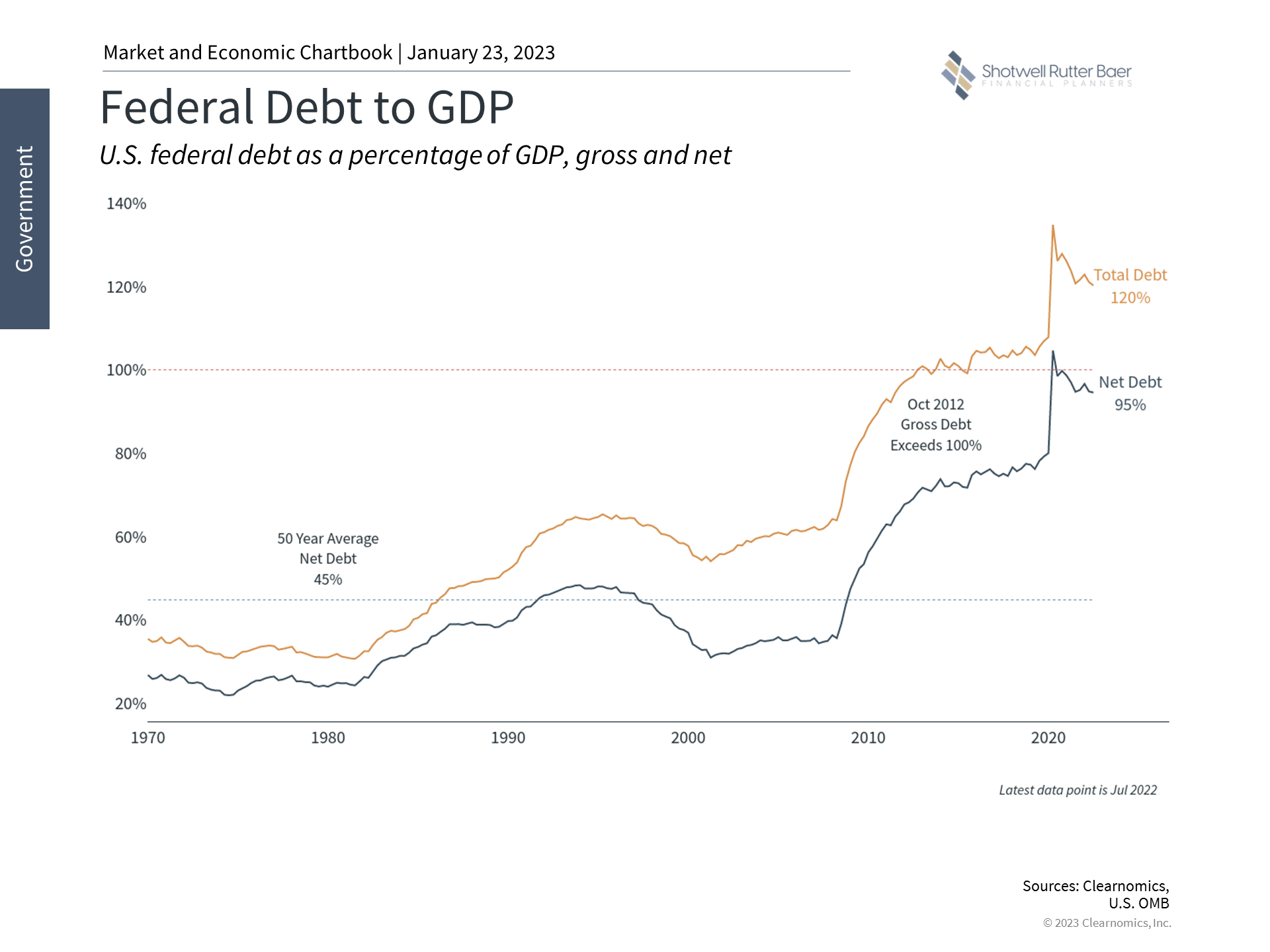

The large and ever-growing national debt is a controversial topic that impacts the economy and markets in complex ways. At its core, budget deficits occur when the government spends more than it collects in taxes and other sources of revenue, adding to the total debt each year. Even though tax revenues increase as the economy grows (even without raising tax rates), they have been outpaced by spending over time. These expenditures have grown across “mandatory” programs such as Social Security and Medicare as well as “discretionary” items such as defense and education, and have only accelerated since the global financial crisis in 2008 and the pandemic in 2020. The difference between revenues and spending is funded by government borrowing, i.e., by issuing Treasury securities.

What makes this discussion challenging is that several complex issues are intertwined. First, the question around the debt ceiling is not about government spending per se, since that spending has already been authorized through the normal budget process. The only question around the debt ceiling is whether the government can pay its bills. This is akin to signing the papers for a new car and then afterward requesting an increase to your credit card limit. For most of us, the decision to buy something can’t be separated from whether we will pay for it, even if it’s with debt. Unfortunately, the Congressional process for approving a budget by September 30 each year is separate from whether the Treasury can actually pay the bills.

This nearly reached a breaking point in 2011 when a political standoff around the debt limit led Standard & Poor’s, a credit rating agency, to downgrade the U.S. debt. During this period, the stock market fell into correction territory with the S&P 500 declining 19%. Ironically, the prices of Treasury securities increased during the 2011 debt ceiling crisis because, even though these were the exact securities being downgraded, investors still believed they were the safest in the world at a time of heightened uncertainty.

The debt ceiling was eventually raised to $16.4 trillion which averted a government default. Debt ceiling standoffs have occurred a few times since then with the limit suspended and raised in 2013, 2014, 2015, 2017, 2018, 2019, and 2021. Fortunately, despite the headlines and investor concerns, these episodes had little long-term impact on markets. The U.S. has never defaulted on its debt, and nearly all economists and policymakers agree that doing so would lead to turmoil in the financial markets and increase borrowing costs for businesses and everyday citizens.

The government has run budget deficits throughout history

Second, debt ceiling aside, the national debt at today’s level means that it has more than doubled over the past decade and, with very few exceptions, has grown nearly every year over the past century. While this is often framed as a partisan issue, the unfortunate reality is that neither party has addressed the problem over the past decade. The last major effort was the bipartisan Simpson-Bowles commission in 2010 which had little lasting impact on reducing government spending. The last balanced budgets occurred during the Clinton years and the Nixon administration before that.

Given how heated the topic of government spending can be, it’s important for investors to distinguish between their political feelings and how they manage their portfolios. In other words, investors should focus on what they can control in order to differentiate how things work from how they would like them to.

The unfortunate reality is that deficits are unlikely to go away. And yet, despite how unpalatable this may be too many, markets have done well regardless of the exact level of government debt and taxes over the past century. In fact, as unintuitive as it might seem, the best times to invest over the past two decades have been when the deficit has been the worst. These represent times of economic crisis when the government is engaging in emergency spending, which tends to coincide with the worst points of the market. And while this isn’t something investors would hope is repeated often, it does underscore the importance of not overreacting to fiscal policy and politics in one’s portfolio.

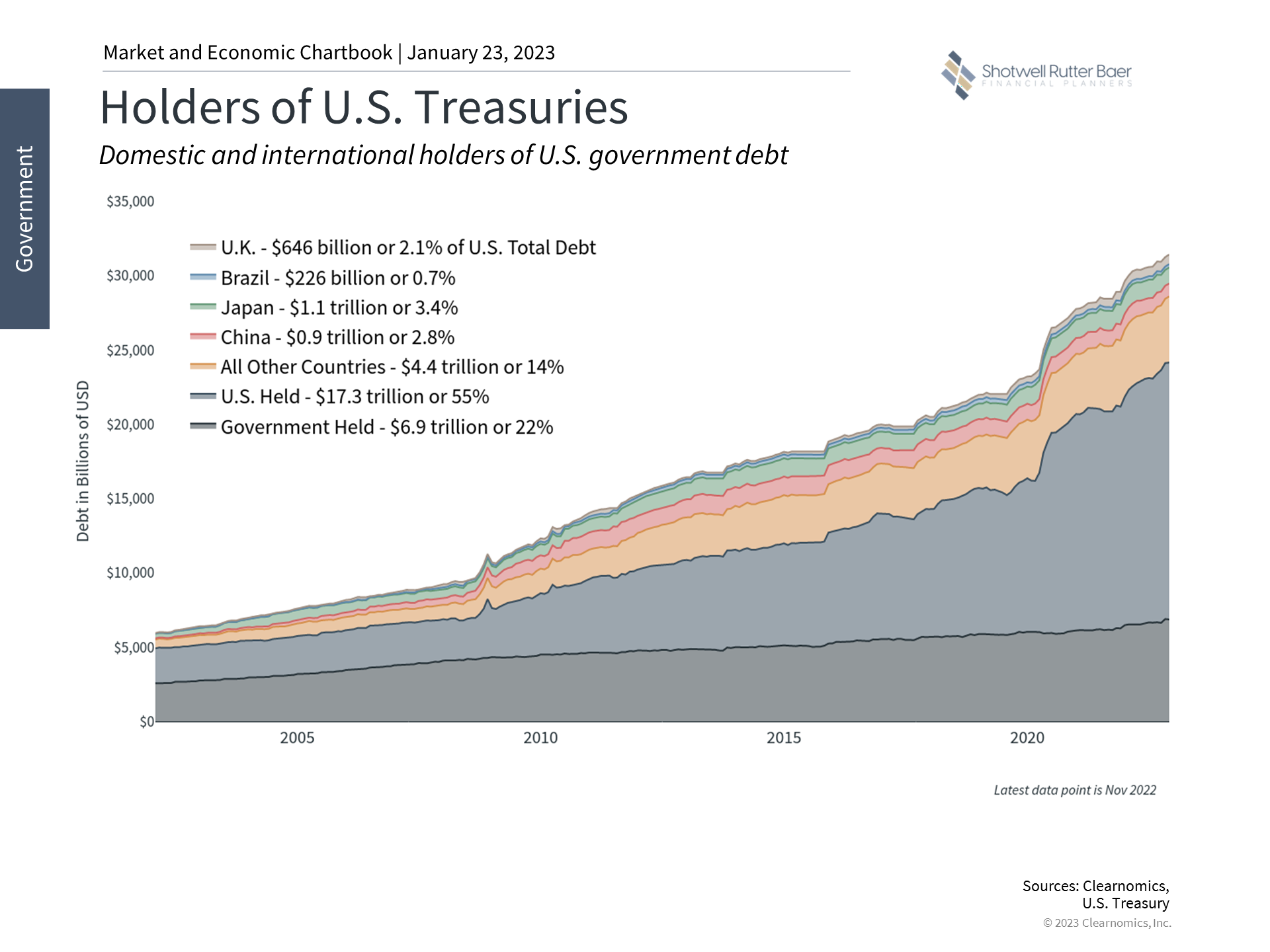

Most Treasuries are held domestically

Finally, many investors worry about who holds U.S. debt – and what this may mean financially and geopolitically as the debt grows and interest rates rise. While it’s true that Treasuries are held by other countries including China, since Treasuries are important to the global financial system, about 77% of the national debt is held either by the U.S. government itself or by U.S. citizens. The amount held by U.S. government entities is generally excluded by economists when considering the total size of the debt since this is the equivalent of moving money from one pocket to the other. Thus, the many headline numbers that focus on total debt rather than “net debt,” which excludes intra-governmental borrowing, may not provide the most accurate picture.

That said, many investors worry that growing debt and deficit levels mean that Treasuries could be less attractive in the future. In the extreme, this could hamper the government’s ability to roll its debt, especially given the jump in interest rates. And while this is a possibility, it’s still unclear where the limits will be. Japan, for instance, has been operating with a debt-to-GDP ratio of about 250% for years. And although interest rates have jumped over the past two years, they have also stabilized and fallen over the past several months.

The bottom line?

The debt ceiling and federal debt won’t be resolved anytime soon and there will continue to be media coverage over the next few months. As with many political issues, it’s important for investors to separate their concerns and not react with their hard-earned savings and investments. History shows that staying invested is the best approach to navigating drama in Washington.

About Shotwell Rutter Baer

Shotwell Rutter Baer is proud to be an independent, fee-only registered investment advisory firm. This means that we are only compensated by our clients for our knowledge and guidance — not from commissions by selling financial products. Our only motivation is to help you achieve financial freedom and peace of mind. By structuring our business this way we believe that many of the conflicts of interest that plague the financial services industry are eliminated. We work for our clients, period.

Click here to learn about the Strategic Reliable Blueprint, our financial plan process for your future.

Call us at 517-321-4832 for financial and retirement investing advice.

Copyright (c) 2023 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Podcast: Play in new window | Download